Trends in intelligent automation for insurance

Insurance organizations all over the globe are accelerating their digital transformation efforts.

Hyland's team

Insurance organizations all over the globe are accelerating their digital transformation efforts.

Hyland's team

Insurance organizations all over the globe are accelerating their digital transformation efforts.

That might be even truer in insurance — an industry that tends to have a longer paper trail, yet relies on quick responses. A recent IDC Analyst Brief commissioned by Hyland and Duck Creek found that 42% of documents and files are unstructured or semi-structured. The global firm also estimates the percentage is “much higher in the insurance sector.”

To further complicate things, the file and document formats — from images to audio and video recordings — are growing in number.

For insurers, capturing and retrieving relevant information often is a job for intelligent automation (IA).

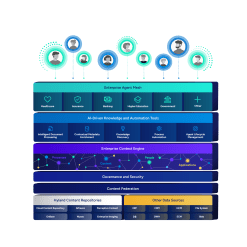

Intelligent automation — the use of automation technologies and artificial intelligence (AI) that anticipates the needs of users and customers while reducing human touchpoints — can take on many forms. In insurance, an intelligent capture and management platform helps with capturing and categorizing documents, and relating these documents and content to each other.

Intelligent automation is a broad term that describes the use of artificial intelligence, machine learning (ML), hyperautomation, document processing and other automation tools to streamline the user experience.

One of those technologies is robotic process automation (RPA). In insurance, RPA can automate customer data collection, claims data collection and background checks to produce faster processes with fewer human touchpoints.

RPA platforms — which readily connect with common legacy systems used by many insurance firms — can also serve as a stepping stone for insurance companies looking to invest in automation technologies.

Download now | Content, automation and AI transformation with Forrester study insights

Artificial intelligence (AI) and machine learning configure and identify data and document patterns.

Information is indexed, and key information is extracted. A crucial step — one that, IDC notes, many insurers haven’t made — is an integrated and intelligent process automation system.

“Integrating document processing with insurance solutions provides a marriage between process activities and the documents they consume and produce at each step in the process,” IDC said in its report. “Processes are more intelligent, and hence, activities and decisioning are more automated.”

The firm’s research shows that 80% of insurers have manual interruptions for more than 40% of their claims cases. The reason: Document management workflows that aren’t integrated with insurers’ core business solutions.

An integrated approach, on the other hand, reduces claims processing times by an estimated 20–35%. That seamless exchange of data among technology solutions results in faster payments to customers — which is as effective of a customer service tool as any.

Learn more | Business process management

Intelligent automation can generate significant changes for insurers. Some of the most crucial are:

Intelligent automation powered by technologies like machine learning, RPA and capture automates manual tasks and improves decision-making and productivity. This leads to faster claims processing and payment approvals.

Freeing employees from repetitive, manual tasks creates opportunities for them to focus on more meaningful work. Staff can focus their time and energy on projects and initiatives that further the organization’s goals.

Workflow and system integration tools automate how information flows through an organization. Human touch points are reduced, and sensitive information is more secure.

Automating records and retention management reduces the risk of human error. Staff can monitor and locate sensitive information as it enters the system, and apply the appropriate action to remain compliant.

— Alan Pelz-Sharpe, A practical guide to intelligent automation

Underwriting, once a manual and paper-intensive process, is being transformed by business processing solutions. Insurers are using content services platforms embedded with intelligence capabilities to automate age requirements, detect signatures and perform important compliance tasks.

A recent Deloitte insurance outlook cited greater use of automation, alternative data and AI as the top three changes insurers need to make in the underwriting process. The switch to intelligent automation in underwriting is in the early stages for many insurers, the global firm says.

Insurers that have made the switch, however, are realizing huge gains.

Deloitte’s research mentions a company that approved 96% of its policies through automated underwriting. Doing so reduced the company’s average turnaround time from 3.8 days to 10 minutes.

“The question is whether most insurers will invest enough to make this vision a reality, at least in the short term,” Deloitte’s outlook says.

For many insurers, the claims management process — from when a claim is first submitted all the way to payment — can be disjointed and slowed by paper documents and manual steps. An innovative content management platform driven by intelligent automation connects each step and reduces the time and money spent on repetitive work.

When a claim enters the system, the information is immediately captured and stored on a secure, centralized electronic repository. One of the best parts: The information is readily available on the day-to-day platforms that employees use.

The number of regulations that insurers have to keep up with can be overwhelming, especially if done manually.

An enterprise content management platform can help insurers stay compliant by aligning people, processes and technology. Leveraging intelligent automation tools makes such processes as validating policies, creating defensible audit trails and generating regulatory reports more efficient and less prone to errors.

Intelligent automation can be a driver for digital transformation in insurance, as well as for organizational change. Insurers can automate the entire policy management process — from creation to communication, management and maintenance.

Insurers that leverage the right technology to solve challenges are able to address such new opportunities as capturing unmet customer needs and expanding core offerings.

More intelligent, more efficient and better for the customer — sounds great, right?

These claims aren’t too good to be true. Here’s a case study that leverages automated intelligence.

The setup:

Funeral Directors Life Insurance Company had eight staffers who were responsible for settling more than 2,000 contracts each week. As claims picked up and new business accelerated, employees were staying past close to process contracts and reduce lag time.

Already users of OnBase, a Hyland content services platform, all it took the FDLIC team was a “Hack Week” and Hyland’s robotic process automation (RPA) solution to automate new business processing. During its five days of innovation and fun, FDLIC figured out how the Hyland RPA and OnBase integration could improve its processes.

The result:

Within a few weeks, FDLIC added five bots that were integrated with Hyland’s platform; to automatically surface information and settle new business contracts.

A month later, the company had an 88% return on its bot investment and a total elimination of lag time in line-of-business processing.

The bots allow the company’s workers to focus on building relationships with customers and producing quicker, more accurate outcomes.

Implementing RPA meant FDLIC’s claims department began to save about seven minutes and $4.36 per claim. Also significant: The insurer saved 20,000 hours in manual processes and its claims volume increased by more than $15 million over a two-year period.

Interest in AI and machine learning is as prevalent as an insurance spot during a football game. But effectively and intelligently capturing critical business information is as important to an insurer as a star quarterback is to an NFL team.

Organizations, AIIM says, can no longer “afford the luxury of manually identifying and categorizing incoming information.” AIIM’s report on intelligent capture, which includes a significant number of responses from insurers, recommends that organizations view AI and machine learning in two contexts.

The first is traditional: how the tools are being used and could be used to improve efficiency and gain insight.

The second is more complex: how the tools can be used to make information more understandable by the machines.

The latter, AIIM says, is “done by adding context to unstructured information — i.e., content.”

Top-performing companies, the association found, are pushing the envelope on AI and machine learning much more aggressively than average organizations. AIIM says the difference in the percentage of large-scale implementations of intelligent capture technologies between top performers and average organizations is “at least” 20 percentage points.

What’s your first thought when you read or hear about intelligent automation in insurance? Does it have to do with human workers being replaced by bots?

The reality is intelligent automation empowers employees to focus on high-value tasks, which leads to increased job satisfaction and an improved customer experience.

Research has shown that intelligent automation can:

Insurance workers today are focusing on emerging technologies, while gaining new skills and responsibilities. They are, in fact, more valuable than ever.

You’ve seen — or read about — the benefits and results IA can produce. But how do you implement IA at your organization?

Alan Pelz-Sharpe, an IT analyst and the founder of Deep Analysis, says to focus on these seven steps:

You can listen to Pelz-Sharpe detail each of the steps in this Hyland webinar.

McKinsey, in researching the future role of artificial intelligence and intelligent automation in insurance, says purchasing insurance will be “faster, with less active involvement on the part of the insurer and the customer.”

By 2030, underwriting as we know it will no longer exist for most personal and small business products in life and property and casualty insurance. More than half of claims activities, meanwhile, will be replaced by automation, the global firm says.

To prepare for what’s ahead, McKinsey recommends that insurers:

The world has seen rapid advancements in technology. The speed of such advances, along with our reliance on intelligent automation, is only going to increase.

Is your organization ready? Hyland, a leading provider of intelligent content solutions with the ability to leverage the power of intelligent automation, can help.